I’ve been a big fan of PolicyMe since it first launched in 2018, so I’m excited to finally share my own PolicyMe review after getting new life insurance policies with them! I loved how they wanted to make life insurance more accessible by providing life insurance online as well as making it more affordable for Canadians. Did you know that according to their recent survey, PolicyMe found that 44% of Canadians don’t have life insurance, 40% of which say it’s because they can’t afford it? More accessible and affordable options like PolicyMe means that more Canadians will be able to get coverage, which for many families can be life-changing.

PolicyMe also prides itself in not over-selling or over-insuring customers since non of their reps work on commission, they only sell term life insurance, and they’ll tell you straight-up if you don’t need any coverage yet.

So when my husband and I bought our new home recently and realized we needed more life insurance coverage, I knew exactly who we would turn to.

My Experience Getting Life Insurance with One of the Traditional Insurance Companies

To give you some backstory, my husband and I both got our first life insurance policies in 2016. We used an insurance broker my husband had used before and bought 20-year term life insurance policies with coverage of $500,000 through one of the traditional life insurance providers. I had just turned 30 and my husband had turned 31, and we’d recently bought our first home together.

Our Previous Policy & Coverage

At the time, we felt like $500,000 was enough coverage for us because we didn’t have that many assets, and our mortgage was just over $300,000. Having this amount of coverage gave us peace of mind that if one of us died, the death benefit would not only cover the entire mortgage but also help the survivor pay for funeral costs and living expenses for several years.

The Approval Process

The process to get this insurance policy was archaic, to say the least (especially by today’s standards). First, we had a long phone call with an insurance broker to discuss our options. Then, in order to apply for coverage, the broker actually had to come into our home and go through all the paperwork with us in-person. After that, a nurse was sent to our home to do a medical exam in which she took blood and urine samples from each of us. Once our application and samples were reviewed and we were approved, our last step was to set up payments for our monthly premiums. That was the last time I’d really thought about our life insurance policies…until now.

Why We Got a Second Policy with PolicyMe Instead

What changed was my husband and I sold our townhouse at the end of 2021 and bought a new house with a substantially larger mortgage. This meant that our current policies wouldn’t be enough to cover our entire mortgage or provide anything extra for funeral costs and living expenses for the surviving spouse. So, I decided to go through PolicyMe to get us a second policy to get more coverage.

And in case you’re wondering “Why didn’t you just use your original insurance provider?” That’s a great question and here’s why…

Convenience

First, let’s talk about convenience. With PolicyMe, you can go through the entire life insurance quote application process online in 20 minutes or less (on average), just like it says on their website. It was simple, intuitive, and fast (how it should be!). Not only that, since PolicyMe reviews your application online, you might get approved instantly if you’re an eligible applicant like I was.

Although my original insurance provider has had to go semi-virtual because of the pandemic, it’s still nowhere near as convenient. For instance, in order to get a new or additional insurance policy, you can’t go directly through the insurance provider. You have to go through a broker.

So, I contacted our old broker to get some quotes. From the point of first contact to getting quotes for a few different policy options, it took 3 days. That’s a big difference compared to only 20 minutes!

Cost-Efficient

The cost was another big factor. To give you some context, for our current policy ($500,000, for a 20-year term) we pay:

Me: $23.40/month

My husband: $38.70/month

Combined, we pay $62.10/month.

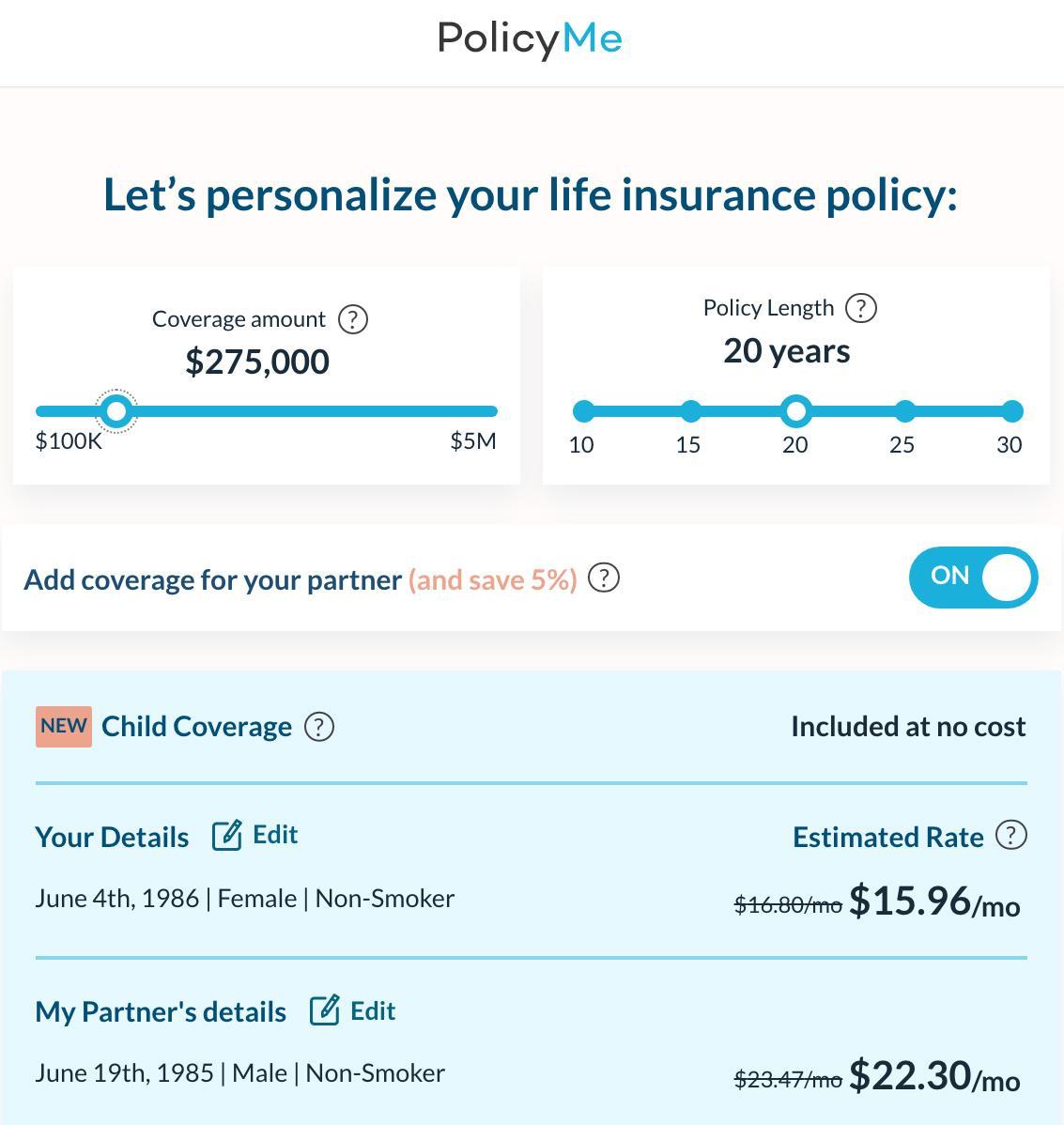

After checking out PolicyMe’s coverage calculator, it determined that in order to be sufficiently protected with our new house, we should get an additional 20-year term life insurance policy with $275,000 in coverage. Here’s the quote I got from them.

PolicyMe Cost

Me: $15.96/month

My Husband: $22.30/month

I should note, that this pricing includes a 5% lifetime policy discount for getting a joint policy with my husband (*UPDATE: Since I wrote this post, they’ve changed the discount to 10% off the first year of the policy).

To compare prices, I asked my broker what the cost for this additional policy would be if we went with our original insurance provider. Here’s what he quoted me:

Competitor’s Cost

Me: $18.56/month

My Husband: $24.75/month

That’s a difference of $2.6/month for me and $2.45/month for my husband.

In other words, if we were to go with PolicyMe, we’d save a combined $5.05/month. That may not sound like much, but remember how small amounts add up to a lot!

$5.05 x 12 months = $60.60/year in savings

$60.60 x 20 years = $1,212 in total savings

Going with PolicyMe would save us $1,212 over the life of our insurance term. Not only that, if we went with PolicyMe and decided to pay annually instead of monthly, we’d get an additional 9% discount to save even more on our premiums. I don’t know about you, but I’d much rather put that money somewhere else like towards our investments.

Another cool thing that PolicyMe provides is free coverage for kids. They provide an additional $10,000 in coverage for each of your kids aged 6 months to 18 years at no extra cost to you. PolicyMe is actually the first life insurance provider to do this in Canada.

Because of these big factors, my husband and I decided to go with PolicyMe.

Now, in case you’ve landed on this blog post because you’re also shopping around for life insurance and are curious about using PolicyMe instead of one of the traditional life insurance companies out there, here are some important things to know.

What to Know About PolicyMe

Who Issues the Policies?

PolicyMe’s policies are issued by Canadian Premier Life Insurance Company, one of Canada’s most reputable life insurance companies.

Do They Offer Permanent Life Insurance?

PolicyMe only offers term life insurance, which can be a good thing if that’s what you want anyway! This means they can’t try to upsell you on an expensive whole life or universal life insurance policy that you may not need.

How Long Does the Approval Process Take?

They say that it takes 20 minutes to complete your application on their website and going through it myself I’d say that’s fairly accurate. They also say that most applicants receive a decision instantly (whereas a traditional insurance provider/broker could take weeks). This is also true since I was approved instantly after filling out my application.

What Kind of Coverage Do They Offer?

They offer policies between $100,000 to $5,000,000 in coverage for people between the ages of 18-75. They also offer terms of 10, 15, 20, 25, and 30 years.

How Do I Know How Much Coverage I Need?

PolicyMe makes sure you get the right amount of coverage (and not too much) by having you answer a series of questions with their coverage calculator. I used the calculator and was happy with what they suggested.

Are There Medical Exams?

Not always, but if you do, no biggie! Remember, I had to get a medical exam for my previous policy and it was honestly not a big deal.

For me, I wasn’t required to do one but it’s on a case-by-case basis. You do however have to allow for the MIB (formerly the Medical Information Bureau) to check your medical records to uncover any errors, omissions, or misrepresentations made by insurance applicants. In other words, you may not have a medical exam to prove that the information on your application is accurate, but you do need to allow them to check your records in order for them to prevent fraud from taking place.

Are There Any Discounts?

Yes! If you and your partner get life insurance policies together, there’s a special couples 5% discount. And if you decide to pay your premiums annually instead of monthly, there’s an additional 9% discount.

Are Children Covered?

Yes! PolicyMe includes $10,000 in coverage for each of your children with your policy, at no extra cost.

Is PolicyMe Available in All Provinces?

Unfortunately not…yet. PolicyMe is available in all provinces and territories except for Quebec, New Brunswick, and Newfoundland. But they are working on being available in these provinces later in 2022!

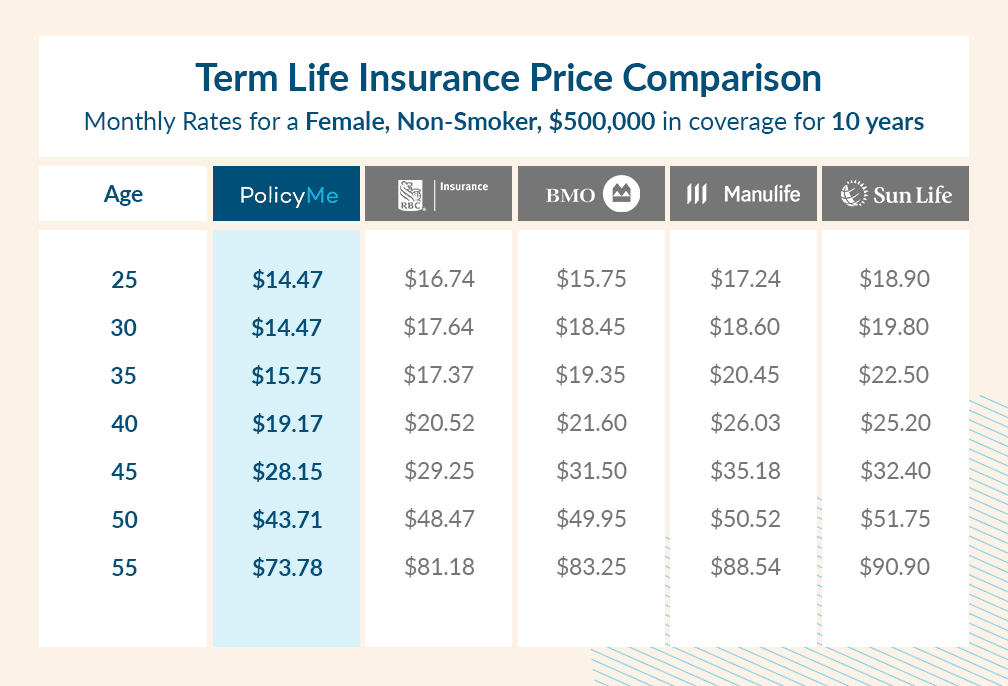

How Do Their Rates Compare to Other Insurance Companies?

As you can see from the charts below, they offer very competitive pricing, lower than most of the main insurance companies in Canada.

What’s Their Customer Service Like?

Customer service is super important, especially when it comes to online-only companies. So I tested it out myself by using their live chat and giving them a call. I was pleasantly surprised by how prompt they were on both. Not only that, I really appreciate the fact that their insurance experts aren’t commission-based so they aren’t incentivized to sell you a policy that’s not right for you just to get a bigger commission cheque.

Am I Safe If They Go Bankrupt?

One question I get often, especially when discussing new fintech companies is “What if they go bankrupt? Will I lose my money?”

Firstly, since PolicyMe doesn’t issue your insurance policy, Canadian Premier does, your policy won’t be affected if for some reason PolicyMe goes bust. But in the case Canadian Premier goes bust too, that’s where Assuris comes in to help.

Assuris is an independent non-profit that was founded in 1990 and every life insurance company in Canada is required to be a member and fund the organization. The purpose of Assuris is to protect policyholders by guaranteeing that you will retain at least 85% of your insurance benefits in case your insurance company fails. But as a reference, there have only been 4 instances where Assuris had to protect policyholders due to life insurance company insolvency:

- LesCoopérants in 1992

- Sovereign Life in 1993

- Confederation Life in 1994

- Union of Canada Life in 2012

PolicyMe Review Final Thoughts

So that’s my full PolicyMe review for 2022. Personally, I had a great experience getting new life insurance policies through PolicyMe for my husband and I, and feel really good about being properly protected in case something happens. But don’t just take my word for it. Check out these other PolicyMe reviews from other customers to make up your own mind.

Thanks for sharing your experience with PolicyMe! It’s always helpful to hear real-life stories when choosing life insurance. Your insights on their application process and customer service were especially valuable. I’m considering them for my own policy, and your review gives me more confidence in that decision!

Great insights! I’ve been considering life insurance options, and your experience with PolicyMe is really helpful. It’s reassuring to hear about the ease of the process and the customer service. I’ll definitely keep them in mind!